Baron Fifth Avenue Growth Fund | Q2 2024

Recent Activity

During the second quarter, we added to 9 existing positions including: Microsoft, Alphabet, Shopify, Adyen, and Illumina. We funded those purchases by reducing 3 existing positions: NVIDIA, Mastercard, and Veeva. The number of holdings in the portfolio increased from 30 at the end of the first quarter to 31 due to Illumina’s spin-off of Grail, a health care company developing a test for multi-cancer detection.

| Quarter End Market Cap (billions) | Net Amount Purchased (millions) | |||

|---|---|---|---|---|

| Microsoft Corporation | $3,321.9 | $6.7 | ||

| Alphabet Inc. | 2,258.7 | 6.7 | ||

| Shopify Inc. | 85.2 | 3.9 | ||

| Adyen N.V. | 36.9 | 1.9 | ||

| Illumina, Inc. | 16.6 | 1.4 | ||

Our largest two additions in the second quarter were Microsoft Corporation and Alphabet Inc. We continued adding to our position in Microsoft. The company continues to make progress in AI, disclosing that 7% of Azure revenue growth in the quarter was driven by AI, about two-thirds of Fortune 500 companies are now using the Azure OpenAI service, that over half of Azure AI customers now also use Microsoft’s data and analytics tools, suggesting a potentially significant pull through from AI to Microsoft’s other offerings, and that GitHub co-pilot (a coding assistant) continues growing rapidly, reaching 1.8 million subscribers (up 35% sequentially). The company also continues to report strong overall financial results with revenue growth of 17% year-over-year at massive scale of $62 billion, operating income growth of 23% and EPS growth of 20%. The revenue growth was driven by Microsoft cloud which surpassed $35 billion in revenues, up 23% year-over- year, and Azure which accelerated 3% sequentially and grew 31% year-over- year in constant currency. We continue to believe that Microsoft presents an attractive combination of a limited risk of AI disruption on the one hand with a potentially material AI tailwinds on the other, through its positioning as the enterprise platform and its relationship with OpenAI.

We also added to Alphabet. The company reported solid financial results with first quarter revenue growth of 15% year-over-year, driven by 14% growth in search, 21% growth in YouTube, and 28% growth in cloud (which accelerated from 26% growth in the fourth quarter). The company has also increased its cost discipline efforts, which drove operating margins to 31.6% (compared to 25% in the first quarter of 2023). With regards to GenAI, while we are cognizant of the potential risks to the dominance of search, we believe that on the range of outcomes, Alphabet remains well positioned through its massive user distribution (9 products with over 1 billion users each), long-standing AI research labs (DeepMind and Google Brain), top AI talent, a solid cloud computing division in Google Cloud, and deep pockets for investing in AI. During the quarter, Alphabet also held its annual I/O conference, where it provided an update on its efforts in AI including: Gemini is now used by 1.5 million developers; model quality is expanding rapidly (e.g., context window is now 2 million tokens of length); the new genomics model, Alphafold 3 can predict structures of molecules and potentially accelerate drug discovery; new TPU6 AI chips has shown a 4.7 times improvement in compute performance compared to the prior generation; and Gemini for workspace is showing early data on a 30% increase in user productivity. Alphabet also has real value in assets such as Waymo, which are not factored into valuation today (and are potentially included at a negative valuation as they currently generate losses, hurting EPS). We continue to believe that the current valuation of Alphabet presents an attractive risk/reward for long-term owners of the business and have therefore increased our position.

We took advantage of share price volatility to add to our position in the commerce software platform provider Shopify Inc., the multi-channel payments solution provider Adyen N.V., and the DNA sequencing tool provider Illumina, Inc. We believe that the stock sell-offs (these holdings were down 14.4%, 29.6%, and 21.9%, respectively) were driven more by near-term investor concerns rather than fundamental issues. Valuation multiples contracted by 16%, 34%, and 24%, respectively. Shopify is investing more in the near term but we believe the investments will have high ROI (see discussion above); Adyen saw volatility with its take rate which spooked investors, but we believe that this is more due to mix rather than market share losses; and Illumina continues to operate in a more challenging part of the cycle which is impacting its near-term results, but we believe its competitive positioning remains solid and DNA sequencing will become a much larger market over time as genetic advancements continue to progress.

| Quarter End Market Cap (billions) | Net Amount Sold (millions) | |||

|---|---|---|---|---|

| NVIDIA Corporation | $3,039.1 | $41.5 | ||

| Mastercard Incorporated | 410.1 | 1.9 | ||

| Veeva Systems Inc. | 29.6 | 0.7 | ||

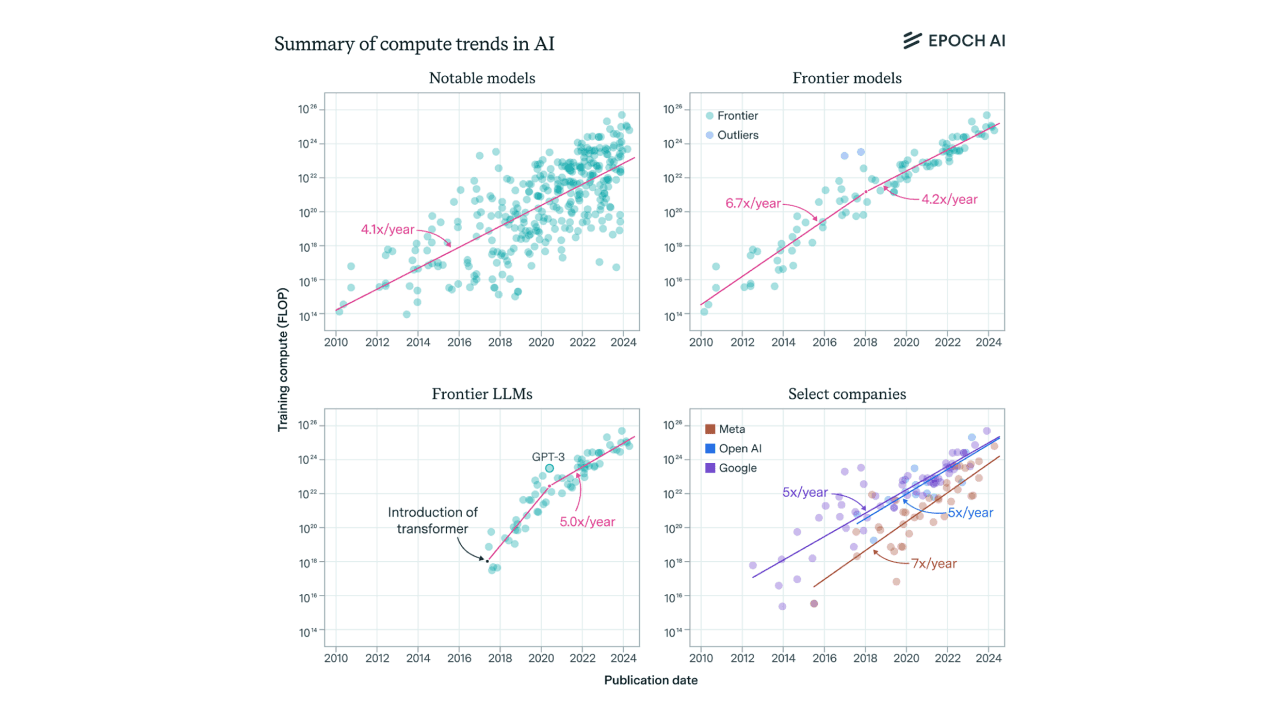

During the quarter, we reduced three existing positions. The largest was NVIDIA Corporation. We would note that our conviction level in the company has not changed although the stock’s incredible recent performance pulled forward some of its future returns, which by definition, tilts the risk/reward equation, prompting us to reduce our position. Nevertheless, NVIDIA remains our largest position in the Fund as we remain in the early innings of AI adoption across industries from health care to automotive, and as the race for Artificial General Intelligence continues. The demand growth curve for accelerated computing remains exponential as newer frontier models continue to get larger and are trained on more data – see graph below6. In addition, as we continue to go down the demand elasticity curve through innovation by NVIDIA and as AI algorithms become more compute-efficient and go up the level of intelligence generated per unit of compute curve, the demand for accelerated computing will continue to grow, benefiting NVIDIA, in our view.

We also slightly reduced our positions in Mastercard Incorporated and Veeva Systems Inc. as the companies continue progressing on their growth s-curves and as we saw a more attractive risk/reward equation elsewhere.

Outlook

As in years past, we have little to offer in the way of a market outlook. Has inflation been tamed? Will the economy continue to slow down? Will we get the three interest rate cuts or none? Trump or Biden or someone else? While these questions are not new, the answers remain elusive, and once they will get answered, other, similar questions will arise. We practice a probabilistic approach to investing and for the time being we expect to continue to operate in an environment where the range of outcomes will remain unusually wide.

Importantly, we do not structure or position the portfolio to benefit from any particular market environment. Instead, we focus on investing in what we believe are high quality business – companies with durable competitive advantages, exceptional management teams with a proven track record of operational excellence and successful capital allocation, and importantly, businesses that we believe have a long runway for growth and an opportunity to become materially larger than they are today.

These companies tend to be leaders in their industries and sell critical products and services to their customers that are hard to replace. That creates stickiness, high switching costs, and pricing power. That enables them to be resilient in the face of macro-economic challenges while continuing to invest in future growth opportunities to take market share and to emerge stronger when the environment inevitably improves.

The rapid advancement of GenAI technology presents both clear risks and compelling opportunities. While the implications of AI on the global economy and on particular industries and businesses are not yet clear, we believe our portfolio includes many companies that are well positioned to benefit from this technological paradigm shift.

Every day we live and invest in an uncertain world. Well-known conditions and widely anticipated events, such as Federal Reserve rate changes, ongoing trade disputes, government shutdowns, and the unpredictable behavior of important politicians the world over, are shrugged off by the financial markets one day and seem to drive them up or down the next. We often find it difficult to know why market participants do what they do over the short term. The constant challenges we face are real and serious, with clearly uncertain outcomes. History would suggest that most will prove passing or manageable. The business of capital allocation (or investing) is the business of taking risk, managing the uncertainty, and taking advantage of the long-term opportunities that those risks and uncertainties create.

We are optimistic about the long-term prospects of the companies in which we are invested and continue to search for new ideas and investment opportunities while remaining patient and investing only when we believe target companies are trading at attractive prices relative to their intrinsic values.

Sincerely,

Featured Fund

Learn more about Baron Fifth Avenue Growth Fund.