Letter from Ron | Q1 2026

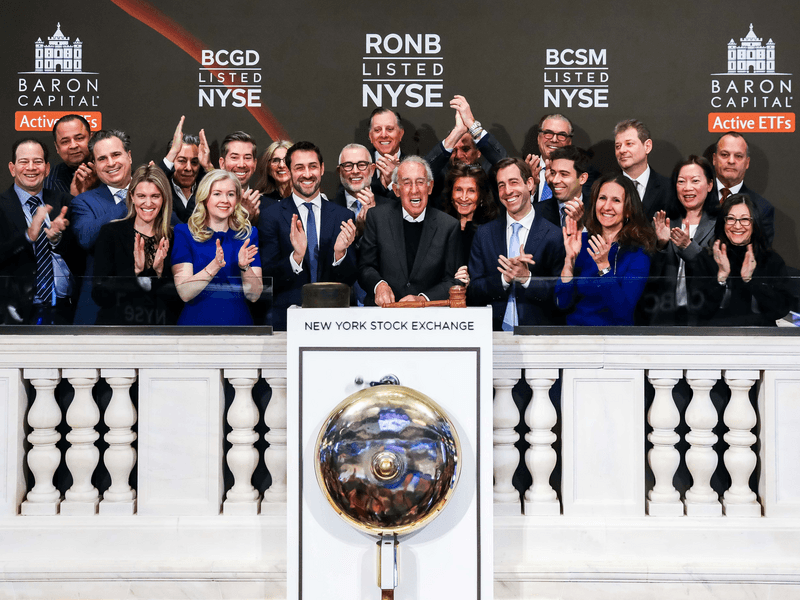

NYSE Bell Ringing Ceremony. Ron and the Baron Capital team rang the opening bell to mark the launch of the first of our Firm's six new ACTIVE ETFs. We considered this a notable event for our Firm that measures time in decades, not trading days. Baron was joined by Lynn Martin, President of the NYSE. My wife was "blown away" by the massive banners hanging outside the exchange welcoming us!!! Thanks, Lynn. December 15, 2025.

Letter from Ron

April 24, 2026 | Download PDF

Baron First Principles ETF is among the first six Active Baron ETFs. "First Principles Thinking," according to GROK, is a physics term used by Aristotle. It means first breaking down an idea or problem to its most basic and undeniable truths. Those concepts, grounded in physics, logic or observable facts, then become the starting point that everything else builds upon. Aristotle treatises and lecture notes. (350-322 BCE)

Elon Musk explains that "first principles" is "a physics way of looking at the world..." According to GROK, that means Elon disregards "that's how it's always been done" thinking. GROK is an LLM, Large Language Model, owned by xAI, a Musk business that was acquired by SpaceX. David, Michael and I are sooo excited about Baron's first ACTIVE ETF, Baron First Principles ETF that the three of us manage. We are also excited about the five other Baron Active ETFs. Baron's "moat" is our Firm's 44-year, exceptional track record. Since their respective inceptions as mutual funds, 15 funds, representing 96.2% of Baron Funds’ AUM have outperformed their benchmarks and 13 Funds, representing 95.4% of Baron Funds’ AUM, rank in the top 20% of their respective Morningstar categories. Six funds, representing 53.9% of Baron Funds’ AUM, rank in the top 5% of their categories... and Baron Partners Fund is the number one performing mutual fund in the United States since its inception as a mutual fund in 2003.*

MISSION:

Changing Lives.

Principles:

"Question Everything"

"Invest in People"

"OWN IT!"

"Exceptional Takes Time"

"Building Legacy"

Before writing this Letter from Ron, I skimmed Goldman Sachs' former CEO Lloyd Blankfein's recently published "Streetwise" autobiography. At a glance, Lloyd's life story is inspiring. I can't wait to read it all. I have been friendly with Lloyd for many years. From the few paragraphs I read, you would definitely conclude his talent, leadership skills, integrity and hard work are what enabled his success.

Perhaps the most important factor we consider before investing in a business is the character of its CEO. One anecdote in Lloyd's story, I think is relevant. In 2008, in the midst of the Great Financial Crisis, Lloyd asked Warren Buffett to invest $5 billion in Goldman Sachs. That was to be certain there could be no question Goldman would survive the crisis.

Warren told Lloyd he would purchase equity in Goldman with one condition. He did not want any senior Goldman executive to sell their shares after Buffett's investment was announced. That was since Goldman stock would certainly rally on the news. Lloyd quickly agreed and promised Goldman executives would contractually agree as well. "I don't need any writings, Lloyd... just your word." So... investing $5 billion to assure the survival of Goldman on a handshake... Speaks volumes of how Warren, an executive renowned for judging people, thinks of Lloyd... as we believe anyone who either knows Lloyd or has read about him would feel. Lloyd sure fits our Firm's algorithm that "We Invest in People."

I also read, at the suggestion of one of Amazon's AWS senior executives, Amazon CEO Andy Jassy's 2025 Letter to shareholders. Jassy described his personal career journey after graduating college as anything but a "straight line." In fact, he described it as a "squiggly line"... since he tried at least seven jobs before graduating business school and joining Amazon. Jassy then outlined the many opportunities Amazon pursued far afield from its original digital bookstore business... and the successful ones Amazon leaned into... and the ones not so successful that were terminated. Further validating the concept that "not a straight line" often produces exceptional results.

A long time ago, in a galaxy not so far away—Central Park, circa 1982—the first Baron Shareholder meeting. Attendees: Ron, David, Michael.

"Long and Winding Road."

The Beatles. 1970.

I moved to New York City in the summer of 1969. That was after four years working as a biochemistry teaching fellow at Georgetown University... and then as a "critical skills," Vietnam draft exempt, Patent Examiner at the United States Patent Office... while attending George Washington Law School in the evenings on scholarship. I dropped out of GW Law after seven semesters with just one to go. My parents were beside themselves. This was because while a patent examiner... and having never taken a college business course... I became interested in a Wall Street securities analyst career. When I moved to NYC, I was unemployed... $15,000 in debt... had $600 in cash... and lived in a high school friend's basement for three months in New Jersey. This while my "day job" was interviewing for a Wall Street analyst position for which I was not qualified. I earned room and board performing errands for my friend's wife on weekends... until I persuaded Tony Tabell at Delafield Harvey Tabell in Princeton that I could learn to be an analyst. Talk about Andy Jassy's straight lines!

The Dow Jones Industrial Average first reached 1,000 in 1966. On March 15, 1982, the Ides of March, which was not so lucky for Caesar... but since challenging historic lore is an element of my optimistic persona... it was lucky for us. After we founded investment firm Baron Capital in the spring of 1982, in August the Dow Jones Average fell to 880! So... investing in an index over discrete periods does not always provide strong performance in every period. One more thing. Baron Capital's book value in 1982 was $100,000... it now is almost $4 billion. My business had just $10 million assets under management in 1982... $100 million in 1992 ... and $54.7 billion at present! We have earned approximately $61 billion profits for our clients... employees... and our proprietary accounts since. This is before SpaceX’s initial public offering at a price likely to be significantly higher than its current private value!!! I try to walk around our office every day and speak with as many of the 231 incredible employees we have hired... trained... and retained. When I do, I am confident that 44 years after our founding... we are just getting started!!! ... and the profits we have earned to date will be exponentially larger in coming decades.

"Buy this... sell that..." Took me a while to learn... not a great idea...

During the 1970s, I earned brokerage commissions as an analyst for my research from hedge funds... mutual funds... business executives... and family offices. Among my stock recommendations then were Federal Express... Nike... McDonald’s... Disney... Tropicana... Golden Nugget... Hyatt... Hyatt International... Manor Care... Choice Hotels... Sea Containers... and Johnson Controls. I learned an important life changing lesson from my investment in the Handy Dan home improvement business owned by Daylin. The two CEOs of Handy Dan, whom I thought were terrific, were fired by Daylin's CEO. Soon afterwards, supported by the prodigious capital raising ability of Ken Langone, the two executives founded Home Depot!!!! But, after doubling or tripling our money in just a few years, I had already sold and missed investing in Home Depot at its formation. Ugh!

Unlike the passive indexes which were essentially flat for sixteen years, share prices of businesses I recommended increased significantly during the 1970s... and afterwards... but since I had trimmed or sold those positions, missed huge opportunities like Handy Dan.

Since I was the original "buy this... sell that" guy... like the investment advisor who advertises on CNBC every week... I was compensated based on commissions in the 1970s. After ten years, the big learning was that wealth is created by buying and holding great growth businesses... not by "buying this and selling that..."

My clients in the 1970s made a lot... and starting from a negative net worth, so did I. Vanguard founder John C. Bogle believed it was not likely individuals could outperform markets and "find a needle in the haystack"... so the best idea, in his opinion, was "buy the haystack." The haystack in this case is the U.S. economy, which is reflected in a passive index fund's portfolio. I did not aspire to be “average” though and have always tried to research special businesses and executives in which to invest. So being a passive investor had no appeal for me.

Just like the 1970s, the passive benchmarks from 2000 immediately before the "Internet Bubble" burst until the lows of the Great Financial Crisis in 2008, declined about 30%! We didn’t earn great returns during those eight years... but our returns were positive... Which proved to me that there is a role for managers who "actively" choose businesses in which to invest. One of my original clients was a famous and highly regarded fund manager. His lesson? "If you discover a great business, it is not possible to own as much as you should." Which is a lesson I try to impart to the individuals younger than I am with whom I work every day. Sure has worked in the case of SpaceX where we have earned 54% CAGR since 2017... and we expect after its IPO to earn 10x-20x-30X its IPO price over the next 15 years! That's from the price of its IPO.

"A contrarian approach is just as foolish as a follow-the-crowd strategy. What's required is thinking rather than polling."

Warren Buffett

I am not aware of other mutual funds or investment partnerships with holding periods so extraordinarily lengthy as ours. As a result, other money managers do not often include information about businesses in which they invest in their literature. That's because their portfolio turnover is generally so frequent that by the time their brochures have been printed, their portfolio companies are no longer owned. We instead treat investments as partial ownership of businesses... not as pieces of paper... or bitcoin... or commodities that you should trade to earn short-term profits.

"Stock prices don’t tell you a lot about a business' long-term growth prospects and whether it is likely to achieve its goals. They only tell you the price at which you can purchase or sell securities on a specific day. In the long term the value of a business will be reflected in its share price."

Ben Graham. Circa 1950s.

Baron Capital’s research is driven by “Baron AI”... our proprietary Analyst Intelligence... Baron AI has been built from decades of firsthand research and tens of thousands of executive interviews. This AI reflects our unique investment philosophy, focused on long-term growth, competitive advantage, and exceptional leadership. Unlike traditional LLMs trained on public data, Baron AI is grounded in proprietary data gathered by our experienced team of analysts. It includes qualitative assessments of management teams’ character, talent and ability. This differentiated dataset enables us to infer what businesses can become over decades. Just as we invest in great CEOs, we invest in our own people, continuously developing and retaining talent whose insights power Baron AI.

Our approach is neither "contrarian" nor "follow the crowd..." According to Bloomberg, "over more than four decades managing money, Ron Baron has heard all the advice. Diversify. Cut losers. Let valuation guide you. He's taken virtually none of it and has achieved a record of success that's the envy of Wall Street."

Baron's Mission to "Change Lives" of our clients and employees by improving their financial circumstances is overriding. We educate individuals to invest for the long term in enduring growth businesses... and to never be afraid. Fundamental research on businesses is determinative. Baron investment decisions are not based on "macro" factors like war... elections... commodity prices... and news ... The only "macro" we consider is... inflation... That is since we regard the continuing devaluation of the dollar as a certainty... which has been the case my entire life. See Table III. Inflation According To Ron.

Baron's analysts attempt to understand the impact of AI to reduce businesses' costs... increase revenues... simplify workflow... and reduce or improve competitive advantages... This research is proprietary and includes company visits and comprehensive analyst conversations with executives. We do not attempt to predict market trends in the short term... nor precisely how AI will change all of our lives. But we do believe it will be a lot.

"Proprietary data is the deepest moat of all."

Henry Fernandez, Founder and CEO of MSCI Inc.

During the second half of 2025 through the first quarter of 2026, share prices of many non-cyclical, recurring revenue, software businesses in which we have significant investments fell substantially. This was as brokerage analysts and hedge funds concluded nearly all software businesses would be disrupted by incredibly fast growing LLM startup businesses... and many consistently growing very profitable businesses with very valuable proprietary data that could not be easily replicated would cease to exist. Those investors believed software businesses would ultimately fail whether or not they own unique and proprietary operational data... their executives are talented... they provide mission critical services... and their businesses’ growth rates are increasing... They believe this is due to AI boosting revenues and lowering costs. Further, their clients are signing long contracts... as long as ten years... at progressively higher rates!

This was as traders propagated a narrative that AI would disintermediate profitable consistently growing software businesses... whose valuable proprietary data was 100% accurate. For highly regulated financial businesses, including insurance, historical data with no "hallucinations permitted"... is super important.

During the past several months we have spent a significant amount of time speaking with and visiting executives and engineers of these software businesses... researching and challenging our prior assumptions. We have also spent a lot of hours prompting GROK... Anthropic... and Gemini foundation models about near- and long-term prospects for these businesses. When short sellers made substantial bets against these businesses believing they might not even exist in the not-too-distant future... valuations fell dramatically. Since we reached favorable conclusions about their prospects we joined those businesses which were in the process of significant share repurchases and increased our holdings materially. Those investments now represent about 20% to 25% of several Baron funds’ portfolios. Those investments were purchased at what we believe were very attractive prices.

Among them... Verisk... Guidewire... Morningstar... MSCI... Interactive Brokers... Spotify... Shopify... Gartner... FactSet and CoStar.

"You knew more about our businesses and their prospects than any other analyst... and I'm not talking about our earnings for the next quarter."

Steve Wynn. Founder Wynn Resorts and Golden Nugget.

"In the 1980s, you were the most curious shareholder of Wynn Resorts. You always asked questions that no one else asked... and were attentive. You really wanted to get into it. No one else was as inquisitive or asked as many questions that were so unusual and interesting to me... which I suppose is why you were so successful investing in my business... and made more than $1 billion profits.

"Ron remained an investor in Wynn for more than 27 years as we expanded in Las Vegas, New Jersey, China, and Boston. Few other investors had the patience and foresight. His firm's investment in Wynn was not swayed by market volatility and ’macro‘ news.” Steve Wynn. Founder and Former CEO. Wynn Resorts. Speaking at the 16th Annual Baron Investment Conference. 2008.

Baron Capital News

- April 1, 2026 SpaceX filed a "confidential S1" with the SEC. This filing, according to historical precedent, contemplates SpaceX' initial public offering before mid-summer. The financial press has reported that lead underwriters Goldman Sachs, JP Morgan, Morgan Stanley, Citi, and BAML have publicly suggested a $1.75 to $2 trillion business value at the company's IPO. It's current value as a privately owned business approximates $1.25 trillion. Reportedly, SpaceX could raise more than $70 billion on this offering. This would be the most ever raised on an IPO. If the offering is as successful as speculated, Baron’s SpaceX holdings, currently valued at $15 billion, according to Bloomberg and others, could reach $24 billion at the time of its IPO!!!! Remarkably, we believe we could earn 10-20-30X the value of those investments in the 10-15 years post the company's planned IPO.

- Baron Generational Growth Fund..."The Mutual Fund formerly known as Baron Growth Fund" is a nod to the Artist formerly known as Prince..." Baron Generational Growth Fund is a high conviction strategy invested in founder-led, family-controlled, entrepreneur-managed business that are initially small- and mid-sized growth companies. Like Baron, also a family-owned business, Baron Generational Growth Fund has outperformed since inception by OWNING businesses for the long term... not trying to time markets by buying and selling those securities. We believe the businesses in this portfolio will endure for generations. They are not being run by professional managers who scrimp on investing in their businesses to boost short-term profits, upon which their compensation is often based.

As of June 1, we will have the ability to continue to invest in these businesses as they grow beyond the small- and mid-cap range which better aligns with our philosophy as long-term investors and our mission of Changing Lives.

On March 30, 2026, I was one of three portfolio managers nominated by Morningstar for the 2025 US Morningstar Award for Investing Excellence: Outstanding Equity Manager. We consider this an Academy Award for investing. Very cool. When I was informed that a Causeway portfolio manager, one of the other two nominees was the winner, it made me think of the real Academy Awards. "May I have the envelope please"... which is then opened on stage and the winner announced. The cameras then zoom in on the nominees who lost and who are expected to applaud and smile. To console me, one of my friends emailed, "Don't worry, Ron, I still think you have a bright future."

Ron at SpaceX launch. Boca Chica, Texas.

- The 2026 Baron Conference will take place on November 6, 2026, at The Met Opera House on the Lincoln Center Campus in New York City. Gwynne Shotwell, President and COO of SpaceX, will visit for the third time to discuss on stage with me the prospects for SpaceX and then answer questions from some of our 5,000 attendees. The goal is a teach-in for the latest and newly public Elon Musk business. SpaceX, due to its 54% annual appreciation since 2017, has become Baron's largest holding... and we believe will become dramatically bigger in the next 10 to 15 years. We've made $13 billion from our $1.75 billion SpaceX investment, which we initiated in 2017. We believe, in public markets, SpaceX will become orders of magnitude larger. Elon, by the way, has appeared at our annual meeting three times also. Once physically. Twice virtually.

- $20 billion of the $61 billion profits we've earned have come from our investments in Tesla... SpaceX... and xAI... all businesses founded and led by Elon Musk. Our investment in Tesla, currently valued at $4.7 billion, could appreciate at least five times in the next 10 to 15 years... and Baron's SpaceX investment presently valued for $15 billion as a private company... could be valued many multiples higher and become at least 10 to 20 times its IPO price within 10-15 years. We invested in SpaceX before rockets were reflyable... before 10,000 Starlink satellites... before Starshield which protects the Homeland... before the dream of one million compute AI data centers in space... and before communication from your mobile phones to satellite was possible... We purchased most of our Tesla holdings 2014-2016... when it was just beginning to produce Tesla cars... before FSD autonomous driving... before its robotaxis... before Tesla Optimus robots. I thought it was so cool in 2014 when Tesla told me how to have my car park itself when I wasn’t behind the wheel. I couldn't imagine that the car would ultimately be able to drive all by itself. Tesla is now Baron's second largest holding. It has increased in value by about 40X since our original purchases.

Thank you,

TABLE I. Baron Funds and Select Accounts Holdings in SpaceX and Tesla (As of 3/31/2026)

SpaceX | Tesla | Fund Returns (%) |

|

| |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Fund | Cost ($M) | Value ($M) | % of Net Assets |

| Cost ($M) | Value ($M) | % of Net Assets | YTD | Since Inception Annualized | Since Inception Cumulative | Inception Date | Net Assets ($M) | |

| Baron Partners Fund | 110.2 | 3,890.3 | 37.4 |

| 95.9 | 2,399.6 | 23.1 | (5.3) | 15.6 | 14,154.4 | 1/31/1992 | 10,394.5 | |

| Baron Focused Growth Fund | 105.0 | 821.1 | 21.2 |

| 11.1 | 231.5 | 6.0 | (5.0) | 13.8 | 4,681.1 | 5/31/1996 | 3,872.1 | |

| Baron AssetFund | 78.5 | 844.7 | 25.5 |

| — | — | — | (7.8) | 11.0 | 5,559.5 | 6/12/1987 | 3,312.7 | |

| Baron Opportunity Fund | 41.0 | 248.4 | 15.4 |

| 15.5 | 87.4 | 5.4 | (8.9) | 10.1 | 1,130.9 | 2/29/2000 | 1,617.0 | |

| Baron Global Opportunity Fund | 15.0 | 172.4 | 20.5 |

| 6.6 | 10.4 | 1.2 | (4.8) | 12.2 | 394.4 | 4/30/2012 | 839.3 | |

| Baron Fifth Avenue Growth Fund | 16.0 | 50.4 | 7.5 |

| 16.0 | 27.6 | 4.1 | (10.4) | 10.1 | 722.1 | 4/30/2004 | 669.7 | |

| Baron First Principles ETF | 25.0 | 30.0 | 12.6 |

| 43.3 | 37.8 | 13.6 | (8.5) | — | (9.2) | 12/12/2025 | 238.5 | |

| BaronX | 919.4 | 4,506.8 | 99.4 |

| — | — | — | 24.6 | 61.0 | 707.6 | 12/1/2021 | 4,531.9 | |

| BaronX II | 441.5 | 1,027.8 | 98.1 |

| — | — | — | (0.2) | 170.3 | 519.1 | 6/11/2024 | 1,047.7 | |

| Baron USA Partners Fund | 26.5 | 413.6 | 79.2 |

| 2.6 | 77.2 | 14.8 | 11.2 | 21.6 | 54,012.8 | 12/1/1993 | 522.3 | |

|

|

|

|

|

|

|

|

|

|

|

| ||

| Baron Capital Group Holdings | 2,043.7 | 14,930.3 | 28.9 |

| 321.9 | 4,436.3 | 8.6 |

|

|

|

| 51,729.7 | |

Additional Must-See Resources (As of 3/31/2026)

Table II. Baron Capital's Top 25 Holdings

Table III. Inflation According To Ron Baron

Table IV. Baron Funds (Institutional Shares and Benchmark Performance)